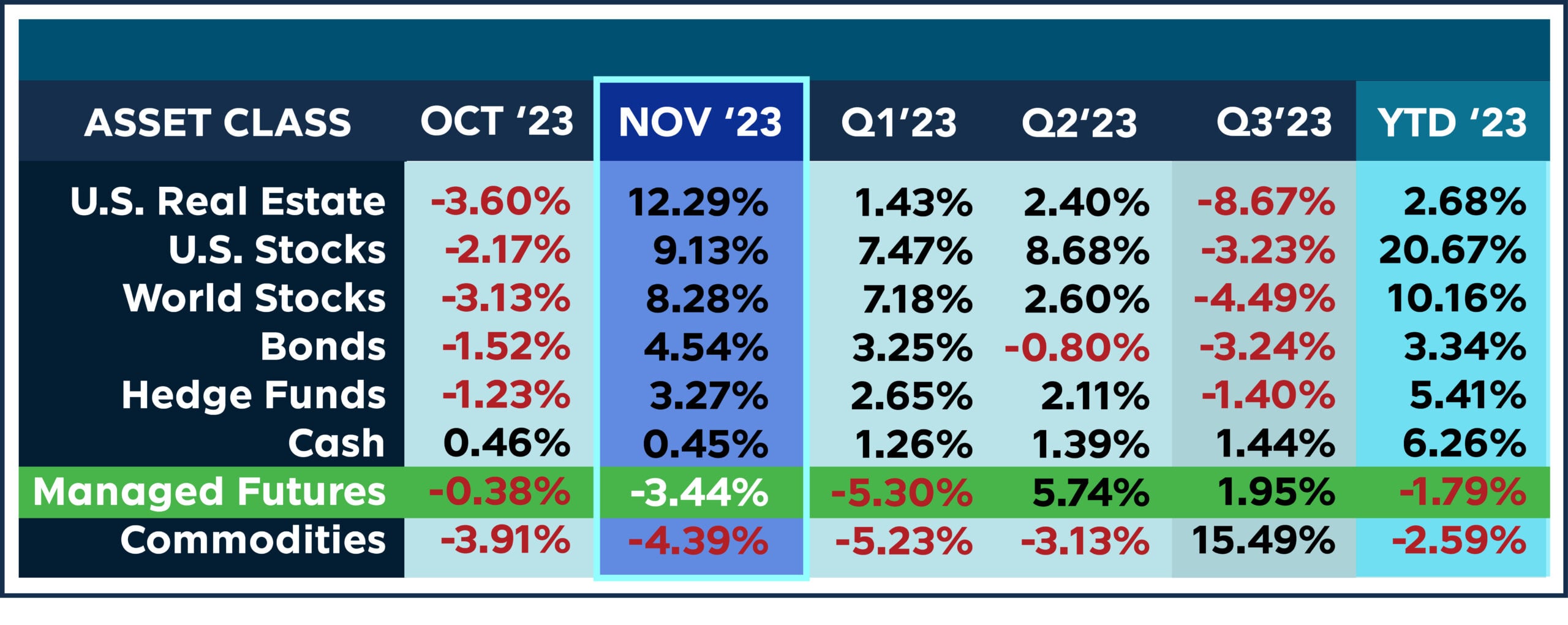

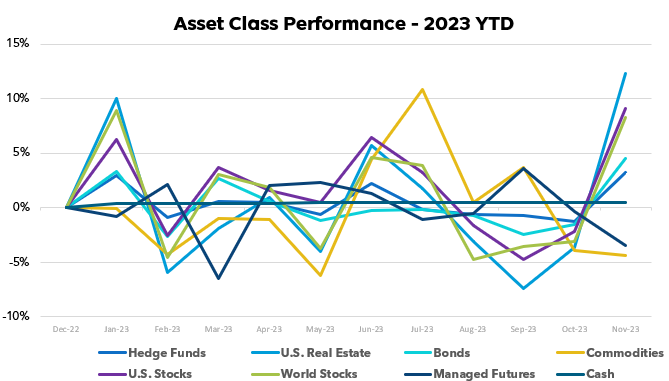

BOOM! And here we go – quite a change this November as we saw several asset classes book gains as easing inflation pressures lifted investor sentiment. Real estate investment trusts powered ahead by 12.29%, signaling strength in the property sector. Domestic stocks also shot up 9.13%, while developed international markets rose 8.28%, demonstrating a renewed appetite for risk.

Fixed income also rebounded strongly as yields declined. The Bloomberg Aggregate Bond Index returned 4.54% for the month. Hedge funds posted their best monthly return of the quarter at 3.27%, effectively capitalizing on shifting dynamics.

Commodities underperformed, however, declining -4.39% as demand softened for industrial materials. Meanwhile, managed futures struggled with the sharp reversal in stocks and bonds, losing -3.44% on the month.

Looking ahead, diversification across investment approaches remains rewarding amid ongoing macro uncertainties. Signs of peaking price pressures lifted opinions broadly across markets. But as always, time will tell how conditions continue evolving.

Past performance is not indicative of future results.

Past performance is not indicative of future results.

Sources: Managed Futures = SocGen CTA Index,

Cash = US T-Bill 13 week coupon equivalent annual rate/12, with YTD the sum of each month’s value,

Bonds = Vanguard Total Bond Market ETF (NYSEARCA:BND),

Hedge Funds = IQ Hedge Multi-Strategy Tracker ETF (NYSEARCA:QAI)

Commodities = iShares S&P GSCI Commodity-Indexed Trust ETF (NYSEARCA:GSG);

Real Estate = iShares U.S. Real Estate ETF (NYSEARCA:IYR);

World Stocks = iShares MSCI ACWI ex-U.S. ETF (NASDAQ:ACWX);

US Stocks = SPDR S&P 500 ETF (NYSEARCA:SPY)

All ETF performance data from Y Charts