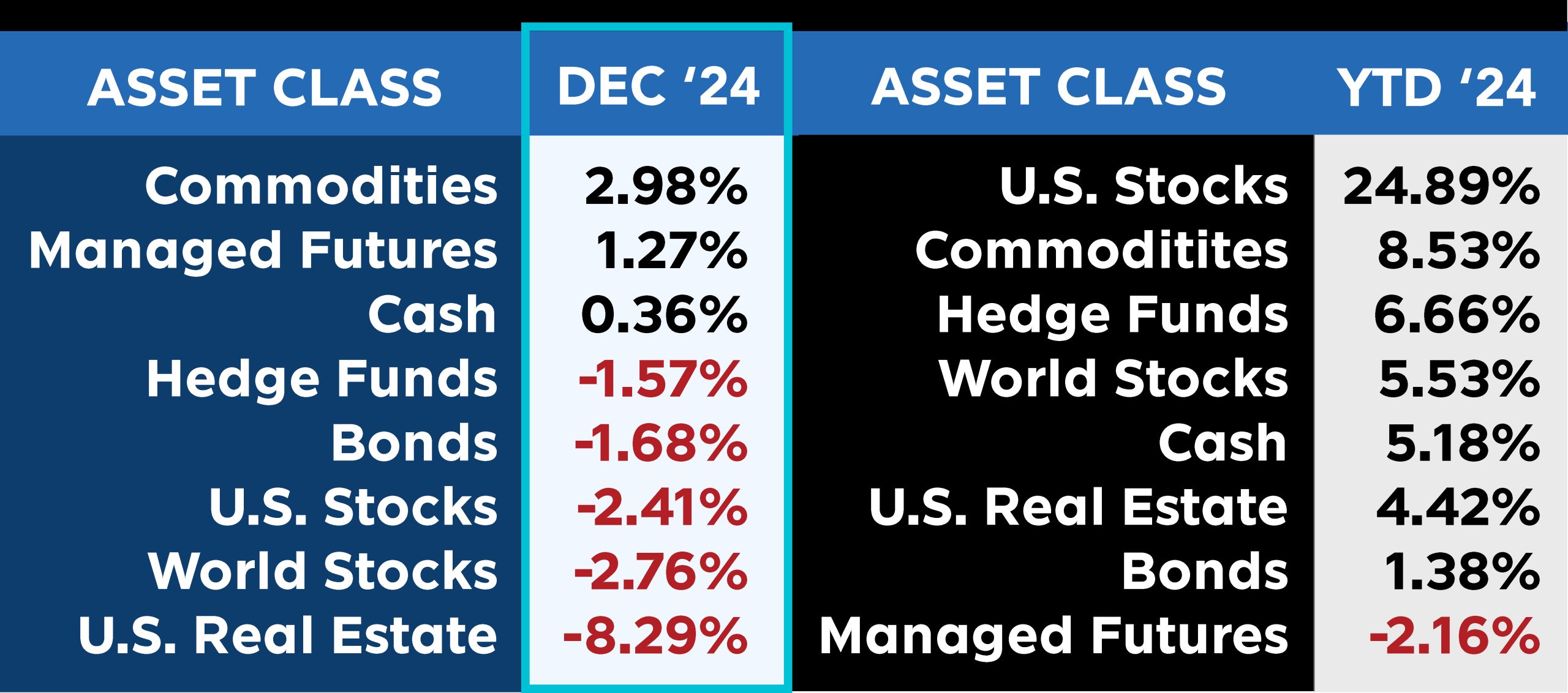

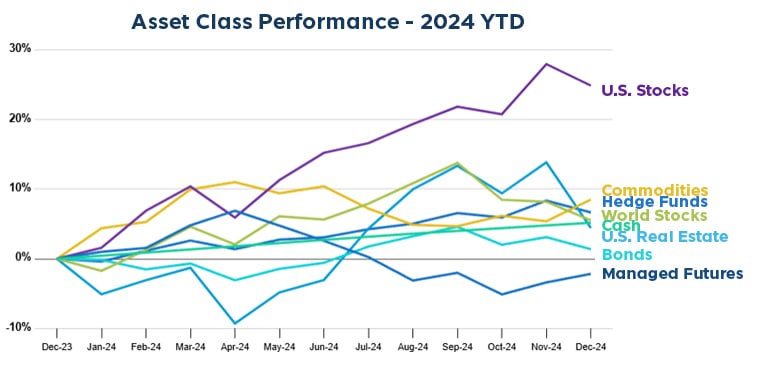

As the final whistle blew on December 2024, the asset class scoreboard showed a tough month for most players, with only a few bright spots. Managed Futures showed some resilience, posting a solid gain of +1.27% in December, although that was mainly a bounce back from a down month in November. Elsewhere, most other asset classes struggled to stay afloat. Commodities also managed to finish in the green with a +2.98% gain, recovering from November losses. However, the rest of the field faltered, with U.S. Real Estate taking a particularly hard hit, dropping -8.29% as interest rates spiked, and U.S. Stocks and World Stocks losing -2.41% and -2.76%, respectively.

December’s performance capped off a challenging Q4, which saw U.S. Real Estate, World Stocks, and Bonds all underperform. Looking back at the year, all we can say is it was a bit of a ‘meh’ year for everything except US Stocks (and only a handful of names, at that). How long can that continue is the big question as we begin 2025.

Past performance is not indicative of future results.

Past performance is not indicative of future results.

Sources: Managed Futures = SocGen CTA Index,

Cash = US T-Bill 13 week coupon equivalent annual rate/12, with YTD the sum of each month’s value,

Bonds = Vanguard Total Bond Market ETF (NYSEARCA:BND),

Hedge Funds = IQ Hedge Multi-Strategy Tracker ETF (NYSEARCA:QAI)

Commodities = iShares S&P GSCI Commodity-Indexed Trust ETF (NYSEARCA:GSG);

Real Estate = iShares U.S. Real Estate ETF (NYSEARCA:IYR);

World Stocks = iShares MSCI ACWI ex-U.S. ETF (NASDAQ:ACWX);

US Stocks = SPDR S&P 500 ETF (NYSEARCA:SPY)

All ETF performance data from Y Charts