We read a lot around these parts; it comes with the job, and we always like to come across well put together pieces from outside our offices, enter Eclipse‘s recent paper. It wouldn’t seem like the type of thing we would be into, titled: Combining Momentum and Carry Strategies Within a Foreign Exchange Portfolio.

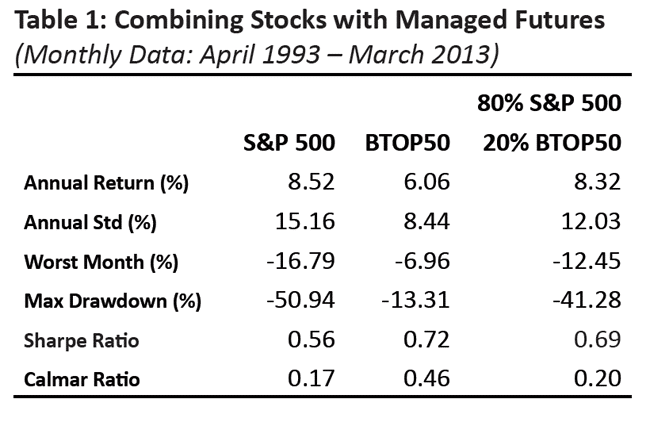

For one, we’re not all that into ‘foreign exchange portfolios’ – seeing people get too carried away trying to get foreign exchange exposure without really understanding what that is or does. Anyway, we liked how the paper starts off, with a nice little table highlighting the benefit of adding 20% managed futures exposure to a stock portfolio. (note it is through Mar. 2013, and still holds true, despite the poor environment managed futures has been in as of late).

Source: BarclayHedge

Source: BarclayHedge

(Disclaimer: Past performance is not necessarily indicative of future results)

But the paper is more than just a managed futures advertorial, the paper is really about exploring the benefits of strategy level diversification, and on a more general level – combining a technical, systematic based model such as trend following/momentum, with a macro/fundamental strategy such as FX carry.

Ahhh, the old carry trade, often talked about but less frequently understood. Eclipse does a nice job of explaining just what the carry trade is, and why it is theoretically profitable.

“Carry is a simple, commonly used strategy in foreign exchange markets that involves buying currencies with higher yields and selling currencies with lower yields. One variation of this strategy can be easily accessed using Bloomberg’s Forward Rate Bias (or FX carry) function. The strategy, as we implemented it, ranks each currency based on that country’s 3-month deposit rate yield and takes long positions in the three highest yielding currencies and short positions in the three lowest yielding currencies. Theoretically, as argued by Burnside, Eichenbaum, Kleshchelski and Rebelo (2011), the carry-trade bears fundamental economic risks and therefore should earn positive expected returns.”

They go into three different ways to weight a portfolio with momentum and carry, finding that equal weighting works the best. And, of course, combining the two together looks better than either do separately (we’ve yet to see any papers when the combined result is worse…) But the interesting thing to us wasn’t really how the combination performed. The interesting thing to us is seeing how the carry trade has performed over the past few years while the momentum trade has been struggling (we’ve added the down arrow to momentum since 2009 and upwards sloping arrow to the carry strategy).

Source: Eclipse Capital

Source: Eclipse Capital

(Disclaimer: Past performance is not necessarily indicative of future results)

This would explain the inclusion of the carry trade in quite a few ‘managed futures’ programs we’ve come across recently. It’s hard to pass up that positive performance of late while the momentum strategy has been struggling, but beware the crisis period with too much carry trade exposure. Just check out 2008 for the carry trade up above – that’s quite the sell off. Indeed, Quest Partners piece from earlier this year showed that the largest managed futures programs (as represented by the BTop50) have become much more correlated to the FX Carry Trade, and warned that this may impact their performance to deliver crisis period performance in the future.

It’s a devil of a dilemma – add something to the portfolio that’s working now, but that may cause problems later… or forego what’s working now in order to maintain the purity of the crisis period performance profile later. Or the third option – try and have it both ways, getting the good from the carry trade now, and timing its exit correctly when momentum comes back into vogue.