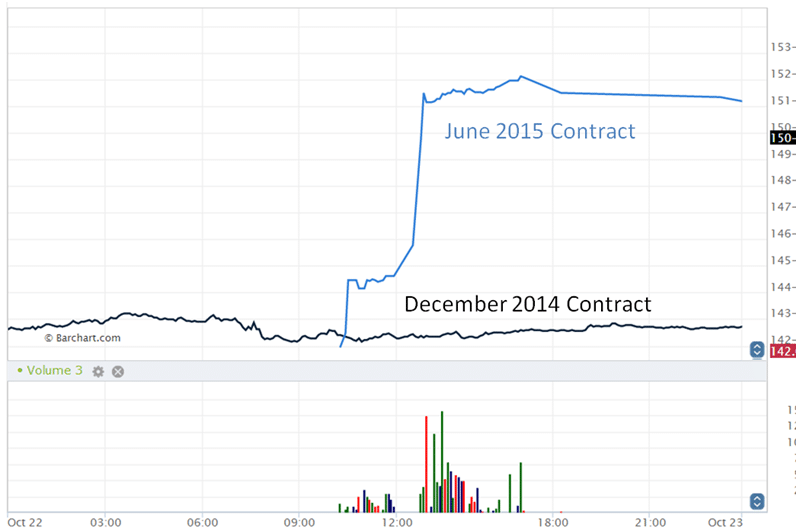

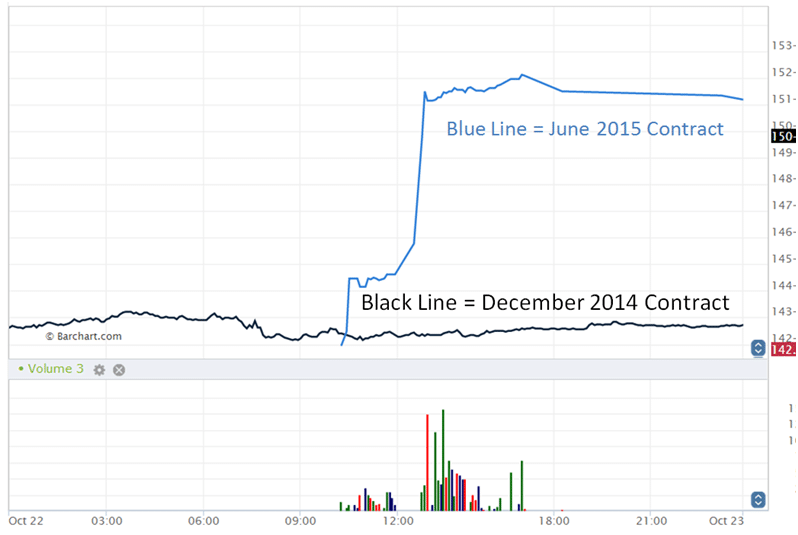

While everyone was watching the US Stock market bounce +5% over the last 8 trading days, there were a few hours of sheer terror/excitement (depending on what side of the trade you were on) in the 30 year US Bond Futures market at 10:00 am hour on October 22nd. What? Say you… I don’t remember any big moves in bonds at that time. And if you were looking at the so called ‘front month’ contract, you would be correct. The December 2014 bond futures traded in a range of 142-10 to 142-12 between 10 am and 1 pm last Wednesday, as you can see below.

But while all was calm in the front month, there was a huge move going on in the June 2015 back month contract. Wednesday was the first trading day for that contract, and it quickly jumped from 141 to 152, a percentage gain of 7%, with a volume of over 16,000+ contracts in just 2 hrs. Compare the two moves below:

(Disclaimer: Past performance is not necessarily indicative of future results)

(Disclaimer: Past performance is not necessarily indicative of future results)

Chart Courtesy: Barchart

Typically a move like that is something you see over a couple weeks, or even a couple months, not a single day, and not by a contract so far in the future. What was going on?

Per Reuters, the reason for the jump wasn’t market volatility, a surprise decision by the FOMC, or some economic report… The move was the results of a decision the U.S. government made more than a decade ago, to suspend the 30 yr bonds because it was running on a surplus and demand was starting to lag.

“What sets these futures apart from others is they’re the first ones where the U.S. government’s decision to stop issuing 30-year bonds from 2001 to 2006 must be accounted for when valuing the derivatives. The size and speed of yesterday’s jump indicates the initial traders of the contracts hadn’t factored in the unusual rules governing these particular products, said Craig Pirrong, a finance professor at the University of Houston.”

The June 2015 contract was the first time the market was taking into consideration the lack of 30 year bonds in the early 2000’s. What?^&% If you’re having trouble making that math work. So did we. It seems like a decision in 2000 on 30 year bonds would affect the bonds 30 years from then, in 2030. Not here in 2014. Well, it turns out this futures stuff isn’t as easy as the ETFs and Alternative Mutual Funds make it look.

You see, the 30 year bond futures contract has at its base a basket of 30 year government bonds, but they aren’t all 30 years from now. In fact, the limit is bonds callable or maturing at least 15 years from now.

Here’s the deliver-ability definitions of the bond Futures specifications from the CME website.

“U.S. Treasury bonds that, if callable, are not callable for at least 15 years from the first day of the delivery month or, if not callable, have a remaining term to maturity of at least 15 years from the first day of the delivery month. Note: Beginning with the March 2011 expiry, the deliverable grade for T-Bond futures will be bonds with remaining maturity of at least 15 years, but less than 25 years, from the first day of the delivery month. The invoice price equals the futures settlement price times a conversion factor, plus accrued interest. The conversion factor is the price of the delivered bond ($1 par value) to yield 6 percent.”

That’s whole lot of jargon. What does this mean exactly? Basically, a bonds futures contract, take June 2015 for example, are bonds with various coupons (return) and maturity dates – the exchange then bundles these together when creating the futures contract. So that contract isn’t one bond alone, but multiple bonds. So the June ’15 bond futures are supposed to have in their basket of deliverables – bonds that are maturing within 15 years from then. 2015 plus 15 years = 2030, which is 30 years after the decisions made 14 years ago…in 2000.

Confused yet? The CME came out with how they’re attempting to resolve this issue, which goes as follows:

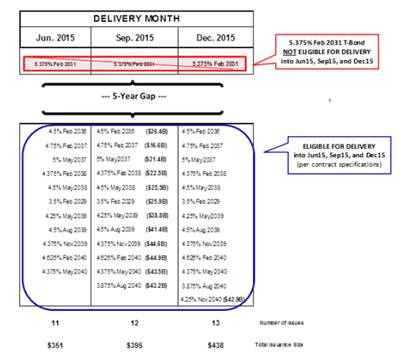

“CME Group announced that the 5-3/8s of Feb ’31 will not be eligible for delivery into the June 2015 (Jun ’15), September 2015 (Sep ’15) and December 2015 (Dec ’15) delivery months, in order to address the five-year term-to-maturity gap in the U.S. Treasury Bond (T-Bond) futures Contract Grade. The five- year gap is the result of the absence of 30-Year U.S. Treasury Bond issuance between early 2001 and early 2006.

Excluding this specific bond from delivery eligibility in these three deferred delivery months will prevent a situation of having a single bond isolated as the five-year gap nears the front of the delivery basket. It will also ensure that the changes have only a negligible impact on the overall size of the delivery basket. The following table shows the baskets that will be modified:

{kind=link}

Still confused? So were all of the traders who used the old math to price the new contract, down at 141. But somebody who had been reading the fine print and knew of this unique scenario saw a golden opportunity – a massively mispriced futures contract versus the underlying instrument. These sorts of arbitrage opportunities don’t last long, and this one lasted just under 3 hours until the market ran up to the correct price based on the correct underlying basket of bonds.

There you have it.