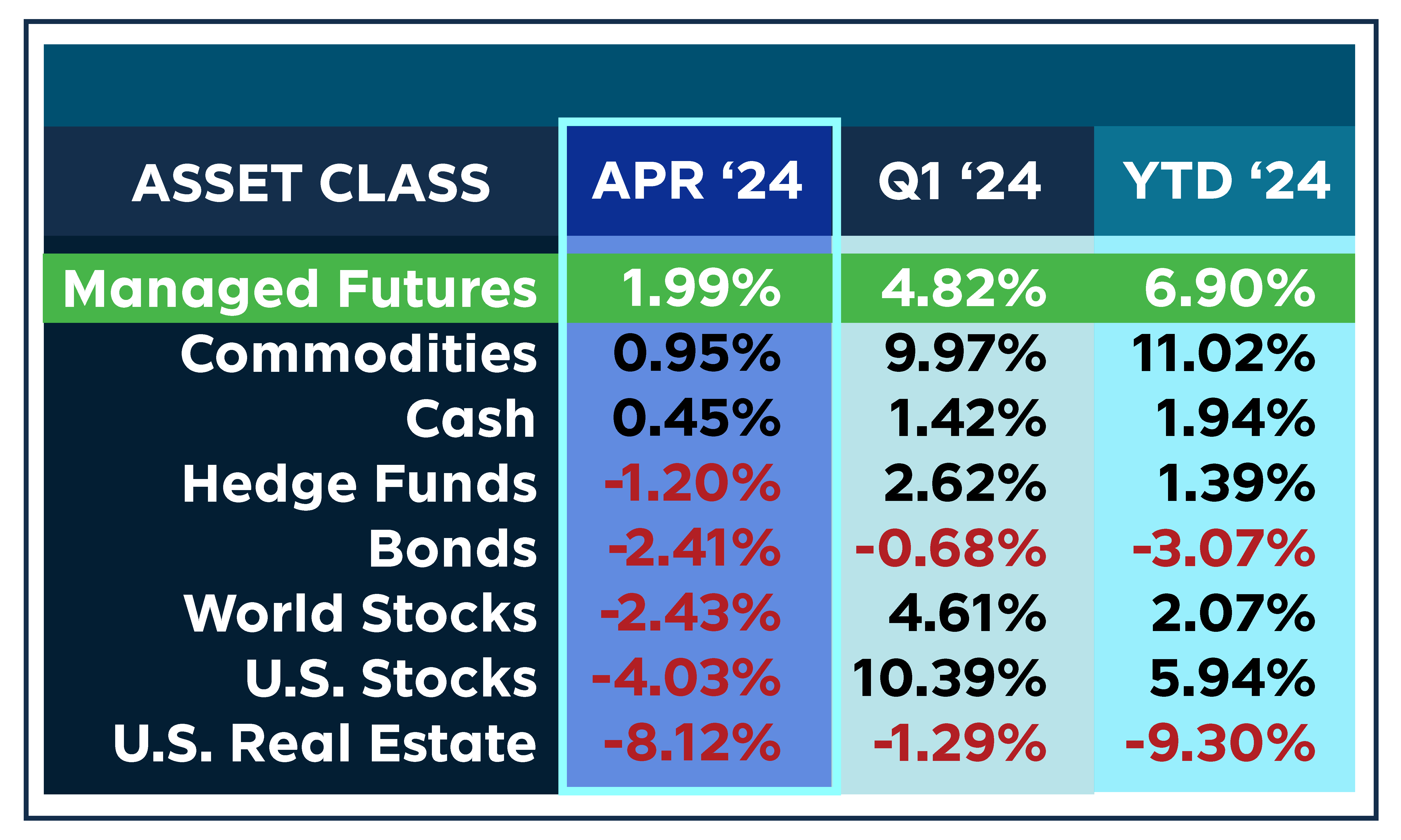

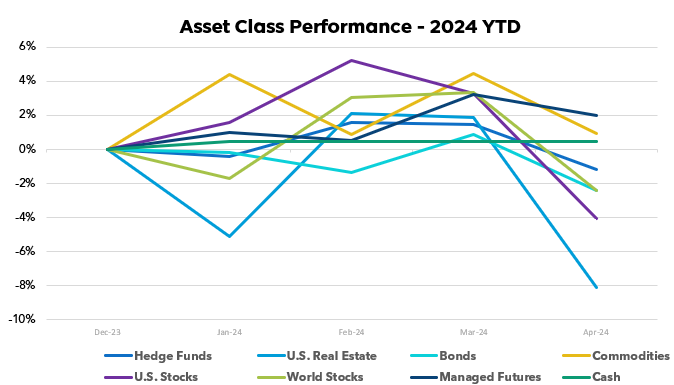

April represented a step back following March’s gains, aside from Managed Futures being the star of the show this month.

Commodities demonstrated resilience, posting a modest +0.95% growth despite the turbulence induced by the prospects of normalizing financial conditions. This volatility led to portfolio recalibration across sectors.

Managed futures strategies once more, demonstrating relative resilience, advancing +1.99% through balanced long-short exposures, and leveraging their flexible framework. Such approaches facilitated careful risk management as conditions fluctuated.

Elsewhere, riskier assets experienced a sharp pullback as economic signals became mixed and policy directives reoriented. This led to significant drops, with Real Estate taking a huge dive(adjustment) of -8.12% and equities dropping -4% for US Stocks and nearing -2.50% for World Stocks. Bonds came in just below those equity drops at -2.41%, with almost every asset hitting their lowest percentage of the year.

April thus painted an incomplete window into 2024’s landscape. Ongoing diversification anchoring a spectrum of investments, including certain non-directional elements empowered to reposition nimbly according to trends, seems apt to smooth returns through fluid backdrops ahead.

Past performance is not indicative of future results.

Past performance is not indicative of future results.

Sources: Managed Futures = SocGen CTA Index,

Cash = US T-Bill 13 week coupon equivalent annual rate/12, with YTD the sum of each month’s value,

Bonds = Vanguard Total Bond Market ETF (NYSEARCA:BND),

Hedge Funds = IQ Hedge Multi-Strategy Tracker ETF (NYSEARCA:QAI)

Commodities = iShares S&P GSCI Commodity-Indexed Trust ETF (NYSEARCA:GSG);

Real Estate = iShares U.S. Real Estate ETF (NYSEARCA:IYR);

World Stocks = iShares MSCI ACWI ex-U.S. ETF (NASDAQ:ACWX);

US Stocks = SPDR S&P 500 ETF (NYSEARCA:SPY)

All ETF performance data from Y Charts